Since mid-2024 the memory market has shifted from cyclical softness into a pronounced supply squeeze: DRAM (system RAM) and NAND (SSD) prices climbed sharply as hyperscalers and AI workloads aggressively expanded demand while available wafer capacity and near-term fab investment lagged. The result: higher contract prices, tighter retail availability for consumer SKUs, and a market that may remain elevated well into 2026 unless capacity ramps accelerate.

What changed: demand shock meets constrained supply

The market dynamics that usually drive memory prices — investment cycles at semiconductor fabs, inventory digestion after previous booms, and consumer PC replacement rhythms — were upended by two forces in 2024–2025:

- AI & data-center demand

Large language models and other generative AI systems dramatically increased memory intensity per server. Training clusters and inference fleets require large volumes of DRAM (including DDR5 and high-bandwidth memory variants) and dense NAND for fast storage. Hyperscalers and AI infrastructure customers have been placing large, prioritized orders and often signing long lead-time contracts, absorbing a substantial share of available production. - Slow capacity response

Building or expanding wafer fabs and memory back-end lines takes years and very large capital outlays. After a prolonged downturn in 2022–2023, many manufacturers paced capex and delayed certain expansion projects. Tool lead times, logistics bottlenecks, and geopolitical export controls on advanced equipment further slow the ability to add near-term supply. That lag turned a surge in demand into an acute mismatch.

Other contributors include suppliers shifting production toward higher-margin products (e.g., HBM and enterprise-grade parts), conversion of some capacity to newer node processes, and a generalized shortage of the older processes that still underpin large volumes of commodity DRAM and commodity NAND.

The evidence: price and capacity signals

Price indices and industry contract notices have shown the memory market moving from modest or declining prices in 2023 to steep monthly increases since mid-2024. Retail SSD pricing tends to lag contract NAND prices because distribution, channel inventory, and finished-goods assembly add friction — but retail SSDs have also begun to climb as component scarcity tightens.

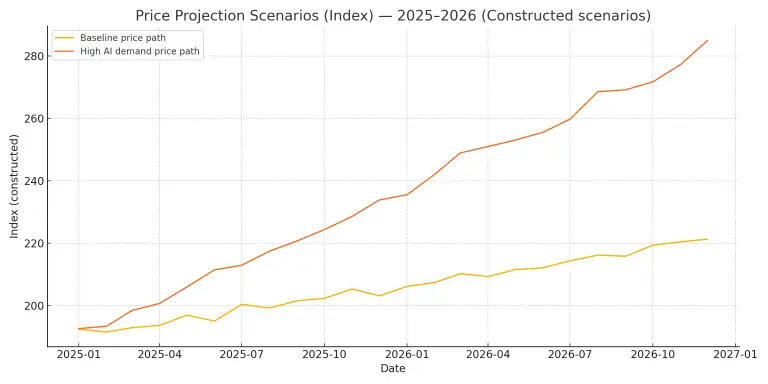

At the same time, estimated wafer capacity growth has not kept pace with the spike in demand. Charts modeling price indices and a simple demand-vs-capacity index show a widening gap beginning in 2024 and growing into 2025, which aligns with public statements from manufacturers and contract pricing reports.

(Chart captions below provide quick context for each figure.)

Short-term outlook (next 12–18 months)

- Prices are likely to remain elevated. Because fab expansions and new production tooling have long lead times, even announced capacity increases often take 12–24 months to materially affect supply. Until that new output comes online, large buyers will continue to soak up available production and keep spot and contract prices high.

- Consumer SKUs may see constrained promotions. Retail discounts and aggressive promotions that were common during inventory gluts will be less frequent. Certain high-capacity NVMe SSDs and higher-speed DDR5 kits could become subject to longer lead times or mini-stockouts depending on vendor allocation policies.

- Manufacturers will prioritize high-margin enterprise orders. Expect suppliers to continue steering scarce inventory to server and hyperscaler customers when necessary; this preserves margins and long-term client relationships at the expense of short-term retail availability.

Long-term outlook (2–5 years)

Two broad scenarios are plausible:

- Normalization if capacity ramps as planned. If manufacturers successfully bring new DRAM and 3D NAND capacity online in 2026–2028 and equipment/geopolitical constraints ease, supply could catch up to demand and prices may return toward multi-year averages. The timing depends on execution of fabs, yield improvements, and whether AI demand growth slows.

- Higher structural baseline if AI demand persists. If AI continues to scale aggressively, memory demand could permanently shift the “floor” for prices higher than the 2010s basin. In that case, memory will become a larger and more stable contributor to semiconductor vendor margins, and cyclical price troughs will be shallower.

Neither outcome is certain — prices will be shaped by how quickly fabs can add capacity, whether suppliers prioritize enterprise vs. consumer demand, and how demand from new AI applications evolves.

Implications by stakeholder

- Consumers / PC builders

If you need to upgrade soon, waiting for deep discounts may be risky. For mid-range purchases, consider buying when you find a good deal rather than delaying indefinitely. Look for bundle deals (system + memory/SSD) which may offer better value than standalone retail SKUs. - Small & medium enterprises

For server or storage purchases, negotiate supply commitments early and consider multi-quarter contracts where possible. Short lead-time purchases can become costly in tight markets. - Enterprises & cloud providers

Continue hedging via long-term agreements and diversify supply sources where possible. Allocate budgets anticipating higher memory component costs and prioritize architectures that optimize memory use. - OEMs & system integrators

Introduce product variants that use slightly lower density or mixed storage options to smooth production and shield customers from the tightest SKU shortages.

Practical buyer advice

- Buy only what you need, but buy with some certainty. If a planned upgrade is essential (workstation, server), secure stock sooner rather than later to avoid price inflation.

- Watch contract-price bulletins from market trackers (TrendForce, etc.) for early signals of price turns.

- Consider alternative timing & warranties. Some vendors offer extended warranties or guaranteed supply as part of premium support and procurement contracts — worth considering if continuity is critical.

Final takeaway

The current memory price surge reflects a structural intersection of surging AI/data-center demand and a supply side that cannot be expanded overnight. For buyers and planners, the period ahead requires prudent procurement, realistic budget assumptions, and attention to contract channels and market signals. If fab capacity accelerates on schedule, relief is possible by 2027–2028 — but if AI demand keeps climbing, memory may settle at a higher long-term price equilibrium than many buyers expect.

Sources & further reading

This article synthesizes industry signals, manufacturer commentary, and contract-price reporting commonly published by semiconductor market trackers and trade publications. For live contract pricing and